General liability insurance is a necessary component of any successful restaurant business. With the policy, you get to pay a monthly premium, so you don’t have to worry about your business being harmed by accidents. This insurance will also assist you in dealing with these issues as they arise, allowing you to focus on running your business.

This is a five-minute guide to help you find out the best providers of restaurant general liability insurance and its cost. It also contains a lot of other ideas you need to know regarding general liability for restaurants.

- 4 best general liability insurance companies for restaurants

- What does restaurant general liability insurance cover?

- How much does general liability insurance cost for restaurants?

- What factors affect general liability insurance cost for restaurants?

- How to find cheap restaurant general liability insurance quotes?

- Other insurance coverages that restaurant may need

4 best general liability insurance companies for restaurants

Many companies offer general liability insurance for restaurants. It can be overwhelming and confusing to find the best one for your restaurant business. We have done the research and here are the top 4 providers of restaurant general liability insurance for your consideration:

- InsurePro: Best for flexible and low-cost coverage

- Simply Business: Best for comparing several quotes and low-cost monthly payment plan

- CoverWallet: Best for comparing several quotes and adding other coverages that restaurants may need

- NEXT: Best for a fast and sleek digital experience and affordable rates

InsurePro: Best for flexible and low-cost coverage

InsurePro is an insurance broker specializing in small businesses. They offer an innovative coverage, which they call on-demand insurance. This means that you don’t need to get traditional insurance coverage for the whole year. You only need to get insurance coverage for any period when you need it, even just a few days. This helps small business owners, including restaurant owners to reduce their insurance cost significantly.

Their approach is all about helping small businesses reduce insurance cost, so even if you get traditional coverage, they try to find the cheapest price for the coverage that you need. That’s the reason why they partner with a lot of insurance companies, which allow them to shop around to find the most affordable price for your restaurant.

They also offer a great digital experience. Within a few minutes, you will be able to get a quote. If you are happy with the quote, you can proceed to buy the policy online immediately. If you need to chat with them to clarify some details, you can choose to chat with them or to just give them a call. They claim that 8 out of 10 customers that choose to call them save an additional 10% on premiums

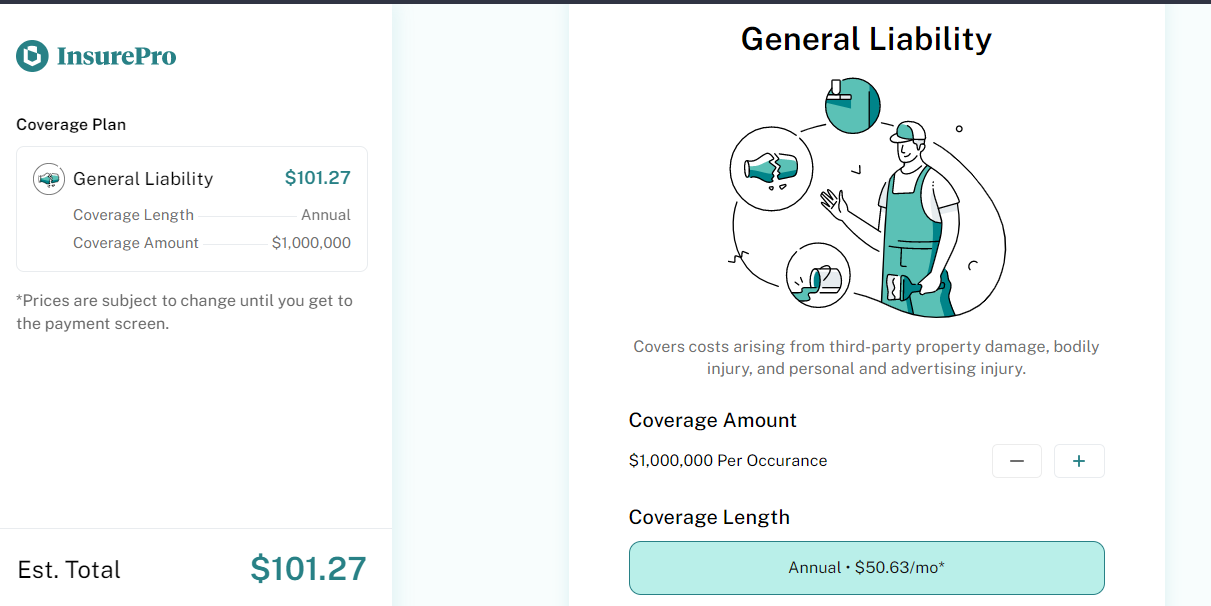

Here is a quote we receive from InsurePro for a small restaurant. As you can see, it is relatively cheap at $50.63 a month for a restaurant general liability insurance policy.

Simply Business: Best for comparing several quotes and low-cost monthly payment plan

Simply Business is another broker specializing in small businesses, including restaurants. If you want to compare several quotes in one place, you may want to start with Simply Business. They work with several leading insurance companies and are able to pull quotes from these companies for you to compare in one place.

In addition, they offer a low-cost monthly payment plan, allowing small business owners to pay monthly, instead of annually without increasing annual premiums. Most companies increase annual premiums by 10-15% in their monthly payment plans, Simply Business does’t. This is a great feature for small businesses trying to save money on their insurance premiums.

CoverWallet: Best for comparing several quotes and adding other coverages that restaurants may need

Similar to Simply Business, CoverWallet is another insuretech broker specializing in small businesses. They also focus on helping small businesses, including restaurants to get and compare several quotes in one place.

The additional benefit of working with CoverWallet is that even you are just looking for restaurant general liability insurance, after you submit your quote request, they will also provide you with options to compare quotes of other coverages that a small restaurant may need such as commercial property insurance or workers comp insurance. That makes it very convenient for small restaurant owners to compare quotes and buy all coverages that they need in one place.

After buying a policy through CoverWallet, you will be able to manage your policies in their digital dashboard with a lot of great features such as downloading the certificate of insurance, filing a claim, or renewing your policy.

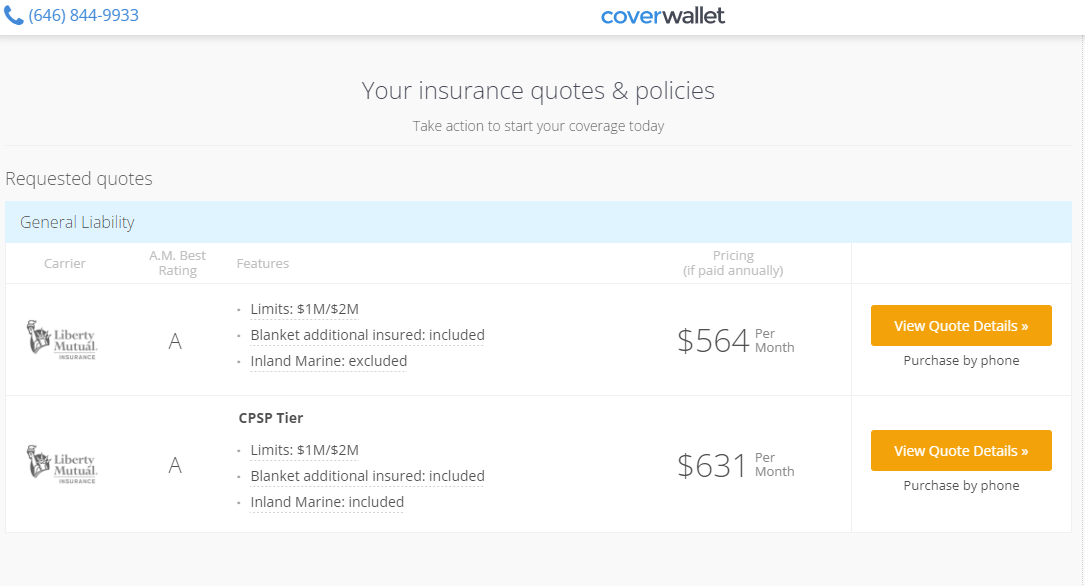

Below is a quote sample that we receive from CoverWallet.

NEXT: Best for a fast and sleek digital experience

NEXT is an insuretech focusing on small business insurance. They build a very fast and sleek digital experience. Within a few minutes, you will be able to get a quote and buy a policy with Thimble.

In our experience, sometimes NEXT offers very affordable prices for their policies, the lowest premiums we can find. However, it is not completely consistent. Sometimes their quotes are more expensive than others.

Since it is so easy and fast to get a quote from NEXT. You may want to give it a try to see if their quote is cheaper than others that you receive from brokers like InsurePro, Simply Business, or CoverWallet.

What is general liability insurance?

General liability insurance or GL insurance is an insurance policy that protects against third-party property damage or personal / advertising damages caused by the owner of a restaurant or an employee.

The policy helps you qualify for leases and contracts while also protecting your small business from the high costs of lawsuits. Considering the importance of the policy, it is usually the first policy purchased by restaurant business owners.

What does restaurant general liability insurance cover?

Commercial general liability (CGL) insurance protects you financially if you’re sued for an injury that occurred at your place of business, causing property damage to a visitor, or causing an advertising injury, such as slander, copyright violation, or libel.

General liability insurance typically covers your legal defense costs if you have a lawsuit. That means attorney, court, and expert witness fees. It may also cover any financial losses you sustain while defending yourself.

General liability insurance also covers your case’s judgments and settlements and the plaintiff’s medical costs.

The following are some specific examples of where general liability insurance can be helpful for a restaurant:

Injuries to customers

Accidents can occur in any restaurant establishment. For instance, your customers slip and fall due to a wet slippery floor. General liability insurance can cover everything from their initial ambulance ride to the cost of their treatment. If the customer files a lawsuit against your business, the policy will also cover you. For injured customers, general liability insurance provides coverage for:

- Court-ordered decisions

- Expenses for funerals in fatal accidents

- Fees for legal representation

- Medical charges

This policy, however, does not cover injuries that may affect your employees. You will need workers’ compensation insurance and your GL insurance to cover employee injuries.

Property damage to customers

General liability insurance covers you when customer property is damaged on your property. For instance, if one of your servers spills a drink on a customer’s tablet, which contains critical business documents, your general liability policy may cover the following expenses:

- Legal fees if the customer decides to press charges

- An out of court settlement

- The price needed to buy a new tablet

Off-site incidents that result in property damage may also be covered by general liability insurance. For example, if your restaurant caters for a corporate reception and your food-warming equipment causes a fire, your policy would cover any subsequent lawsuits alleging property damage.

Host liquor liability

General liability insurance may include host liquor liability insurance in some insurance companies. However, the policy does not cover incidents at a restaurant that regularly serves alcohol. This insurance policy covers bodily injury and property damage caused by the consumption of alcoholic beverages at a social gathering.

If your restaurant has an event where you may serve alcohol, the policy may cover you. This could include company parties with alcohol served or other events unrelated to the company’s profits.

Learn more at the best liquor liability insurance

Advertisement injuries

It is easy to think one has a unique and catchy advertisement phrase. However, many people find out that their lines are not as unique as they think after a while. That may invite lawsuits that will cost you thousands if the line you copied is copyrighted material. In such a case, general liability insurance may cover you.

Generally speaking, general liability insurance will cover any advertising injuries, including the following:

- Infringement of copyright

- Slander and libel

- Written or spoken defamation

If you use adverts to attract customers to your restaurant, make sure your insurance policy covers this.

What doesn’t restaurant general liability insurance cover?

Restaurant general liability insurance covers a lot of risks, but it doesn’t cover everything.

It won’t cover you for the following.

- Employee illnesses and injuries. Workers’ compensation insurance is required to cover employee injuries.

- Accidents involving automobiles. If you own a car, a commercial auto insurance policy financially protects you in the event of an accident while doing business. If you drive a personal car or rent a car for work, you’ll need hired or non-owned auto insurance.

- Professional blunders. You will need errors and omissions insurance (E&O) policy to cover you if you make mistakes while working. Professional liability insurance is another name for an E&O policy.

- Theft and damage to your company’s assets. If stolen or damaged, your business equipment or property will not be covered by general liability insurance. To cover these issues, you’ll need a commercial property insurance policy.

Intentional damages like throwing a computer out the window are not covered by insurance. Furthermore, general liability insurance will not cover deliberate, illegal acts or wrongdoings committed by you or your employees.

How much does general liability insurance cost for restaurants?

General liability insurance costs restaurants less than $120 per month or $1,440 per year for a $1 million per occurrence policy limit. Restaurants are covered by this policy against customer injuries and property damage, and advertising injuries.

Keep in mind that this is just the average. Your rates will be different. Be sure to shop around with a few companies to compare several quotes before making the final decision. We recommend getting online quotes from these 4 companies to compare and select the best and the cheapest one for your restaurant. They all offer online quotes and it shouldn’t take you more than 10 minutes to get quotes from them. You will save a lot of money.

Learn more at how much does restaurant insurance cost

What factors affect general liability insurance cost for restaurants?

Several factors, including the following, determine the cost of insurance for food and beverage businesses.

Alcohol sales and gross sales

The percentage of your alcohol sales compared with your total restaurant sales will affect your policy cost. High-alcohol sales restaurants have higher insurance premiums, especially for liquor liability. Some insurers may not offer you coverage if the alcohol sales pass a certain limit. Similarly, total gross sales affect insurance costs because busy restaurants are riskier.

Staff size

Like gross sales, staff size gives an insurance company insight into a restaurant’s exposure. Carriers will usually consider full-time and part-time employees and annual payroll to check your staff size.

The number of employees determines the cost of employment practices liability insurance, employee benefits liability, non-ownership automobile liability, and employee dishonesty coverage. The more staff you have, the higher you will likely pay.

Property value

Your policy’s cost depends on your property’s value. When offering you insurance for your commercial property, the carrier will likely consider the following to estimate the final value of the building:

- Kitchenware

- Furnishings

- POS computers

- Art

- Signage

- Stock.

The more valuable your buildings are, the more money you will need to insure them.

Business size

Many insurance companies rate restaurants per 100 square feet when determining the premise liability exposure and insurance costs. Larger restaurants have more foot traffic, which increases premises liability risk. Most carriers require indoor and outdoor space when calculating square footage.

Location

Some places in the US are just too dangerous to do business. Some of them are prone to natural disasters, while others have a bad reputation for theft and vandalism in the past. If your restaurant is in these places, be prepared to pay more for insurance. Also, if there is a high cost of hiring lawyers in your area, your premium may be higher.

Industry codes

Not all restaurants are the same. We have cafes, family-style restaurants, casual, fast food, and fine dining restaurants, and all these establishments have different risks. To ensure fairness, the different risks attached to each restaurant type in the industry are defined by the SIC and NAICS codes. Your establishment’s code affects insurance eligibility and premiums. To ensure proper classification, give your insurance broker a clear description.

How to find cheap restaurant general liability insurance quotes?

As a restaurant owner, you must find ways to cut costs. However, you can do a few things to bring down the cost a little bit and save some dollars.

Prevent fire accidents

Your insurer will want to see how you suppress fires when underwriting policies for your restaurant. Because fire is the number one concern for restaurant insurance underwriters, the more fire protection you have, the lower your property rates will be.

Reduce slip and fall injuries

We’ve seen some restaurants with a couple of slip-and-fall claims each year. Insurance companies, on the whole, prefer to avoid these types of claims. If you have procedures to mark wet floors or communicate that you do, you may get a discount.

Keep alcohol sales below 50% of total sales (if possible)

Unless you own a fine dining establishment, keeping your alcohol sales below 50% of revenue will keep you in a lower-cost category. Insurance companies will begin to view you as an alcohol establishment that also serves food if your liquor or alcohol sales exceed 50%.

Combine policies

You need many policies for better coverage, and buying them individually may be expensive. However, if you combine all the policies you need into one policy, you might get paid less for the individual policies.

For instance, if your restaurant is small and low-risk, you may be able to save money by combining general liability with commercial property insurance in a business owner’s policy (BOP). This is less expensive than buying each policy separately. You can add endorsements to your general liability policy or BOP for added protection, such as:

- Insurance for liquor liability

- Insurance for business interruption

- Insurance for cyber liability

Compare insurance quotes for general liability and other policies.

Most people don’t know that insurers differ in terms of how they see risks. That is why quotes differ from one insurer to another. So, before you buy a policy, ensure your check as many as 3 reputable providers and see which one offers you the best bargain.

Here are the 4 companies that we recommend getting online quotes from to compare before making the final decision: InsurePro, Simply Business, CoverWallet, and Thimble. They all offer online quotes and it shouldn’t take you more than 10 minutes. You will save a lot of money.

Other insurance coverages that restaurant may need

While general liability insurance covers most risks restaurants face, it does not provide complete coverage. Restaurant owners should also think about other policies for full protection.

Business Owner’s Policy (BOP)

A business owner’s policy (BOP) bundles general liability and commercial property insurance at a discounted rate. It safeguards your business against customer-related accidents and property damage.

Learn more at BOP insurance cost and the best BOP insurance companies

Commercial auto insurance

Food and beverage businesses that transport food or equipment regularly should have commercial auto insurance. It can cover costs associated with accidents or damage to your company’s vehicles.

Learn more at commercial auto insurance cost and the best commercial auto insurance companies

Workers’ comp insurance

Most states require businesses with employees to have a workers’ compensation policy. If an employee is injured on the job, it may cover medical expenses and a portion of lost wages.

Learn more at workers comp insurance cost and the best workers comp insurance companies

Liquor liability insurance

Liquor liability insurance covers risks associated with serving alcohol, such as an intoxicated customer damaging or injuring another customer’s property.

Learn more at the liquor liability insurance cost and the best liquor liability insurance companies