Caterers face some of the same risks as many foodservice businesses. They also face some unique ones of their own.

- Working around sharp and hot items.

- Carrying trays full of food on slippery floors.

- Working in unfamiliar locations.

The best way to control these risks is to get adequate insurance coverage. This article will explain what you need to know to get the right catering insurance to protect your business, employees, clients, and the people you serve food to.

- 6 best catering insurance companies

- Why do caterers need insurance?

- What types of business insurance do caterers need?

- How much does catering insurance cost?

- What factors affect catering insurance cost?

- How do I get cheap catering insurance?

- Insurance for catering vans

6 best catering insurance companies

- CoverWallet: Best for getting multiple catering insurance quotes from a single source

- Simply Business: Best for an easy application process

- Next: Best for caterers that prefer to do business online

- The Hartford: Best for catering businesses that want to get coverage through a BOP

- State Farm: Best for coverage sold through insurance agents

- Thimble: Best for fast catering insurance coverage

CoverWallet: Best for comparing multiple catering insurance quotes from a single source

CoverWallet makes it fast and easy for busy catering business owners to get several insurance quotes in one place. CoverWallet makes it possible for you to complete a single application, and it checks with its network of insurance providers to get quotes from them. The end-to-end experience typically takes less than ten minutes. CoverWallet is known for:

- Insurance on-the-go

- Fast and easy online application

- Proof of insurance 24/7

- Flexible catering coverage

- Budget-friendly premiums

If getting and comparing multiple quotes quickly is important to you, it could be worth checking out CoverWallet.

Simply Business: Best for an easy application process

Simply Business was founded in 2005. Since then, it’s grown into an insurer trusted by more than 800,000 small business owners.

Simply Business is known for:

- Making it easy to apply for coverage online or to get help from a representative over the phone.

- Allowing you to compare multiple quotes and buy catering insurance in minutes.

- Getting proof of insurance and other documents same day.

- Expert claims support 24/7.

- Being rated 4.7 based on almost 40,000 reviews.

If you need insurance fast and value an easy application process, give Simply Business a look.

Next: Best for caterers that prefer to do business online

Next Insurance is an online business insurance company. Next has an easy online application that makes it possible for caterers to sign up for coverage in minutes. You can purchase business insurance policies individually or in packages customized to particular industries. Next makes it easy for clients to access and share their certificates of insurance and manage their claims online.

One other plus with Next is that you can get up to a ten percent discount if you bundle your coverage with the insurer.

Next is a good option for small business owners who need coverage fast and prefer to do business online. Next is a startup that was founded in 2016. But unlike some other similar startups, Next handles its own claims.

Be aware the if you require highly specialized coverages for your catering business, Next may not be able to provide you with everything you need.

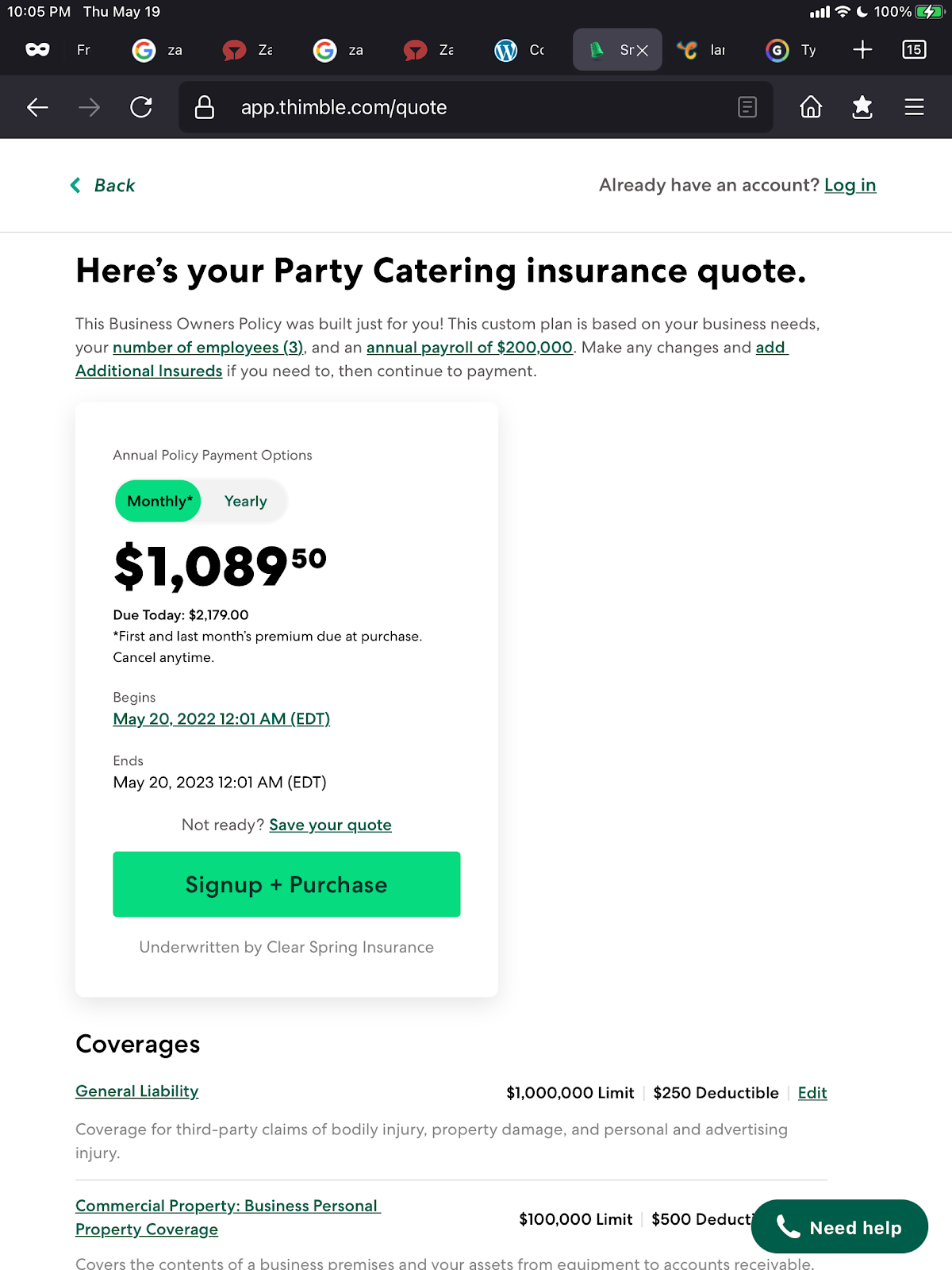

Here is a sample catering business insurance quote from Next. You should notice that the quote Next provided to us below is only for general liability insurance. The quote Thimble provided below for the same catering company is for both general liability and commercial property insurance coverages. This is an area you should pay attention to. Small business insurance premiums vary significantly depending on the coverages you get.

The Hartford: Best for catering businesses that want to get coverage through a BOP

The Hartford is a publicly-traded insurance company. The firm is known for its flexible, customizable business owner’s policy (BOP).

Many insurers only include general liability and property insurance in a BOP, but The Hartford’s has business interruption insurance, as well. This can be a huge advantage to catering business owners because it covers lost income if you cannot offer catering services for a reason covered by your insurance. The Hartford’s BOP makes it easy to add-on other coverages your business may need at reasonable costs.

The Hartford offers a full range of insurance coverage types typically needed by catering businesses. You can purchase coverage from The Hartford through an agent or online. If you apply online, you’ll likely have to complete the transaction over the phone with a company representative.

Catering businesses in Alaska, Hawaii, and New Jersey will not be able to get coverage from The Hartford.

State Farm: Best for coverage sold through insurance agents

State Farm offers a wide range of business insurance policies, from standard coverage like commercial auto insurance to specialized protections certain catering businesses may need.

State Farm may be a good choice for your business if you prefer to get personal help rather than buying coverage online. State Farm sells insurance through a network of insurance agents across the United States. (State Farm insurance is available to caterers in all 50 states and the District of Columbia.) You can’t purchase coverage, or get a quote, unless you work through an agent.

State Farm offers limited online capabilities, including viewing your list of policies and paying your bill. If you get your coverage through State Farm, you have to call your agent if you need service or have to make a claim.

Thimble: Best for fast catering insurance coverage

Thimble is an online insurance provider that sells coverage to people who need catering and other business insurance fast. Thimble does not provide insurance direct. Other insurance companies underwrite its policies.

Thimble is a good option for businesses that need coverage quickly or temporarily. It’s also useful to business owners who hire contractors, as many caterers do. You can use Thimble’s Certificate Manager to determine insurance requirements for the people you’re hiring, and they can then purchase it through Thimble.

With Thimble, you can get a quote and purchase insurance online in minutes. Plus, monthly, daily, and even hourly coverage is available through Thimble.

One issue with Thimble is that it doesn’t underwrite its policies. You’ll have to file claims with the insurer that provides your coverage. Plus, Thimble customer support is only available online. This may not be ideal for catering business owners who prefer to ask questions over the phone, whether when shopping for insurance or after you’ve purchased a policy.

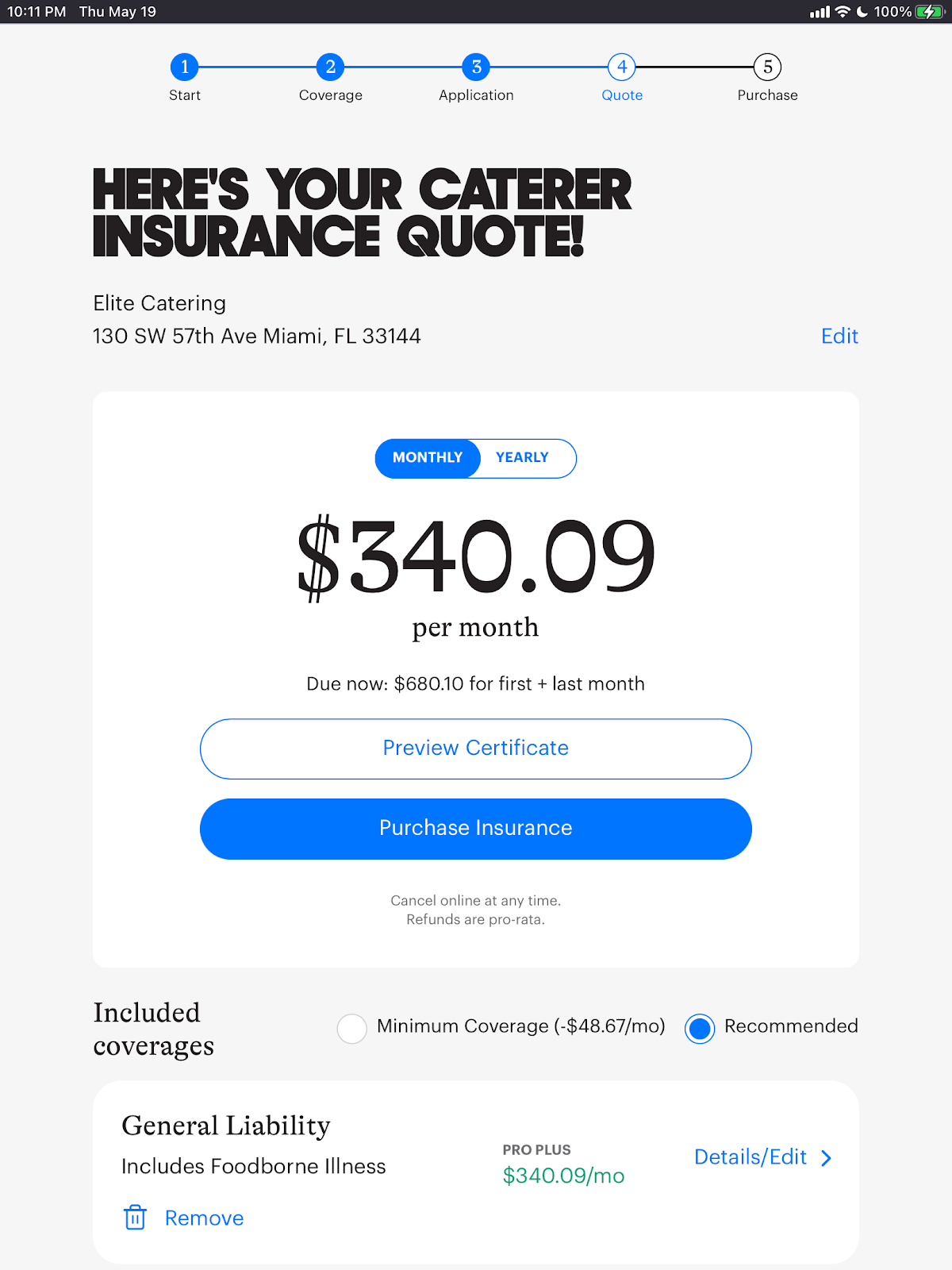

Here is a quote for a small catering company in Miami.

You should notice that the quote Thimble provides above is more comprehensive than the one from NEXT. It includes both general liability and commercial property coverages in one policy.

Why do caterers need insurance?

Caterers are always on the move serving food in new — and often challenging — environments. You’re used to planning for the unexpected.

Catering business insurance does something similar. It helps protect you if something unexpected happens when operating your catering business. It can help pay costs related to personal injury lawsuits, food spoilage, property damage, vehicle accidents, injured waiters, and other incidents.

What types of business insurance do caterers need?

The insurance you need and the level of coverage will depend on your catering business and how it operates. Some coverages typically purchased by caterers include:

General liability insurance

A catering business needs general liability insurance to protect itself from any potential lawsuits that may arise from its services. For example, if a customer is injured while at a catering event, the catering business may be sued for damages. General liability insurance would help to protect the business from having to pay any damages awarded in a lawsuit. Additionally, general liability insurance can help to protect a catering business from other types of accidents or incidents, such as property damage.

Product liability

Catering businesses need product liability insurance to protect them from any legal action that may come as a result of serving food. Product liability insurance covers the cost of any legal action that may come as a result of serving food, including settlements, court costs, and attorney fees. This insurance can help protect your business from costly lawsuits.

In some cases, a catering general liability insurance policy may include product liability coverage, so you may not need a separate product liability insurance policy. While you can save money in this case, make sure you are comfortable with the coverage scope and coverage limit of product liability in these policies since the product liability coverage portion in a general liability policy may be significantly less than in standard a product liability insurance policy.

Liquor liability

Catering businesses should have liquor liability insurance to protect themselves from claims of negligence or wrongdoing related to serving alcohol. This type of insurance can help cover the cost of legal fees and damages if someone is injured or killed as a result of drinking at a catered event. It can also help protect the business if it is sued for providing alcohol to minors or for over-serving guests.

Learn more at liquor liability insurance cost

Business owner’s policy (BOP)

A BOP bundles commercial property and general liability insurance in a single policy. It offers valuable coverage for caterers, protecting against the most significant risks they face. It’s also one of the most economical ways to get these coverages and the easiest way to add on other ones.

- Commercial property insurance covers harm and loss to your business property, including prep kitchens and catering halls, resulting from fire, extreme weather, theft, and vandalism.

- General liability covers injuries that happen to non-employees while on your business property and damage done to other people’s property that occurs while conducting business. It can also protect you against advertising or copyright issues.

In some cases, business interruption coverage is included in a BOP. It covers lost income if you cannot conduct business for a covered reason.

Learn more at BOP insurance cost and the best BOP insurance companies.

Workers’ compensation insurance

Workers’ comp provides benefits for employees who become injured or ill for work-related reasons, a common occurrence for caterers. The benefits include medical coverage, short- and long-term disability, job retraining if the employee cannot return to doing their original work, funeral benefits, and much more. Most states require workers’ comp for catering businesses that have employees. Because caterers often hire temporary or part-time employees, it’s critical that you work with an insurer that understands catering businesses to make sure you have the right level of workers’ comp coverage.

Learn more at workers comp insurance cost and the best workers comp insurance companies

Commercial auto insurance

This coverage helps pay for injuries, legal expenses, and property damage when a catering vehicle is involved in an accident. It also covers vehicle theft and repairs resulting from weather or vandalism. Caterers need to get coverage even if they use personal vehicles as a part of their catering work. Personal auto insurance will not cover accidents when driving for business reasons. For example, if you’re dropping off chafing dishes at an event venue and are involved in an accident, your personal auto insurance won’t cover you.

Learn more at commercial auto insurance cost and the best commercial auto insurance companies

Professional liability insurance

Catering is a complicated business. It’s easy to make mistakes, and clients often sue caterers when errors happen. Examples include serving the wrong food, forgetting to provide a wedding cake, or mixing up the date of an event.

Learn more at professional liability insurance cost and professional liability insurance companies

What is catering liability insurance?

Catering liability insurance is the most popular policy for any catering business. It is one single policy covering all liabilities that a catering business may be exposed to. It is also considered a bundled policy including general liability, product liability, liquor liability, and in some rare cases professional liability coverages. In some cases, a customized general liability insurance policy for catering businesses should serve the same purpose.

If your catering business wants to participate in a big event, it is very likely that the event organizer will require you to have catering liability coverage.

How much does catering insurance cost?

A small catering business pays an average of $95 a month or $1,140 a year for a Business Owners Policy (BOP). Larger catering businesses will pay more. Similarly, one that handles small dinner parties will have lower premiums than one that owns a major catering venue.

The average price above is just for one common policy, Business Owners Policy, that almost all small catering business should have. If you add more coverages, you will pay more.

Even just one policy, this is just the average, your own rates for a BOP will be different. Be sure to shop around with a few companies or work with a top broker like CoverWallet, Simply Business, ez.insure, or commercialinsurance.net to get and compare several quotes in one place to choose the best one for your business. Getting a fast quote on Thimble is also a good idea. It shouldn’t take you more than 5 minutes to get a quote on Thimble website.

Learn more about the details of catering insurance cost

What factors affect catering insurance cost?

Factors that impact the cost of catering business insurance include:

- Foods and services offered

- Business property and equipment

- Business income

- Business operations

- Types of insurance purchased

- Vehicles, their value, and how much they’re used

- Policy limits and deductibles

- Insurer and how it calculates premium rates.

How do I get cheap catering insurance?

It’s relatively easy to get coverage. However, making sure you are not over paying for your catering insurance isn’t always straightforward. Below are a few tips for your to save money on your catering insurance:

Compare several quotes before settling on the final one:

Always shop around for at least 3 quotes before making your final decision. Get quotes online when they are available. Get a quote on Thimble website shouldn’t take you more than 5 minutes. Work with top broker like CoverWallet, Simply Business, ez.insure, or commercialinsurance.net is a good way to get and compare several quotes in one place since the brokers can pull quotes from several providers at once.

Make sure you get the right coverages to protect your catering business

Don’t buy the coverages that you might not need. For example, if you don’t serve alcohol as part of your catering business, you shouldn’t get liquor liability coverage in your policy. If you don’t have full time employees, you might not need workers comp insurance.

Safety-first operation

Make sure you follow all safety standard and practices in your catering business operation. Have the right safety manual at the right place at your business location. Always follow safety procedures when you work with a few clients.

Get the right coverage limits and deductibles

Coverage limits and deductibles affect the premiums of the policy. Reduce coverage limits to the proper level to protect your business or increase deductibles to the level appropriate for your situation can reduce the premiums.

Insurance for catering vans

Catering vans is operating a catering business in a van or a truck. As you can imagine, catering business has its own complications. Now you bring the operations of a catering business into a van or a truck, you basically double the amount of complications and the risks it is exposed to. A catering van definitely need proper insurance coverage to protect itself. There can be several coverages that it needs and it may cost even more. Some of the coverages may be required by law like commercial truck insurance.

Learn more about the coverages catering van would need, how much it costs, and the best providers of catering van insurance.

Catering insurance quotes online

The best way to make sure you don’t over-pay for catering insurance is to compare several quotes to choose the cheapest one for your business. The best way to compare several quotes is to get catering insurance quotes online. Many companies offer catering insurance quotes nowadays, we have done the research and here are the best companies for catering insurance quotes online for your consideration:

- InsurePro: Best for pay-per-day catering insurance quotes

- Simply Business: Best for finding low-cost catering quotes

- CoverWallet: Best for comparing several quotes online

- Thimble: Best for catering businesses that hire part-time employees

One-day catering insurance

If you work part-time in your catering business, you don’t need regular or full-time catering insurance coverage. You just need insurance coverage when you have a job. In such cases, you can get one-day catering insurance policy. Sometimes, it can also be referred to as one-time catering insurance or catering insurance for one event. They all mean the same thing: on-demand catering insurance coverage, ie. only when you need it. The coverage protection is exactly the same as the regular catering insurance policy, however, it is only effective for the period that you need it. The benefit is that you only pay a fraction of the cost of regular policy, and yet get the same benefit. We have done intensive research to find the best insurance companies offering one-day catering insurance policy.

Single-event catering insurance

If your catering business has to participate in an event that spans several days, a one-day catering insurance policy may not be sufficient. Getting several one-day catering insurance policies may be too expensive. In that case, you should look for a single-event catering insurance policy. This policy is designed to provide coverage for the entire event, for example, a one-week music festival or sporting event.

Similar one-day catering insurance policies, single-event catering insurance provide liability coverage for your business. It covers claims and lawsuits related to bodily injury, property damage, product liability, in some cases, liquor liability as well.

When buying a single-event catering insurance, you should also get quotes for a standard catering insurance policy since it may be cheaper to buy a standard policy.

Mobile catering insurance

Mobile caterers usually operate in outdoor areas, such as parks or fields. This is because they need to be able to set up their equipment and prepare food on-site. The nature of their business requires them to travel a lot from one location to the next while transporting all of their catering equipment. It is reasonable to assume that their business operations are exposed to a lot of risks. That’s the reason why they need to have mobile catering insurance.

Mobile catering insurance should include general liability coverage, which protects the business from any damages it may cause to third parties. The policy should also include property coverage, which will protect the caterer’s equipment and supplies in the event of a loss or damage. It should also provide product liability coverage to protect them from lawsuits related to their food quality. Lastly, as they are moving from one location to the next, they definitely need to have commercial truck insurance coverage.