If you have a lot of expensive jewelry, you probably already know that your homeowners insurance only covers a small portion of the total cost. You could add a rider to your homeowners insurance, but even that might not cover the full replacement cost of your precious jewelry. You might want to consider jewelry insurance for your expensive heirlooms.

Here are our top seven picks for jewelry insurance in 2021.

Jewelers Mutual: Best Overall

Jewelers Mutual has been insuring jewelry since 1913, which makes it one of the oldest jewelry insurance companies. You won’t have to worry about them going out of business. They cover all major perils, such as theft, loss, damage and disappearance. After all, jewelry is small and can be lost or stolen easily.

Jewelers Mutual earns an A+ rating on the BBB website, and they score an average of 4.8 stars on Trustpilot.

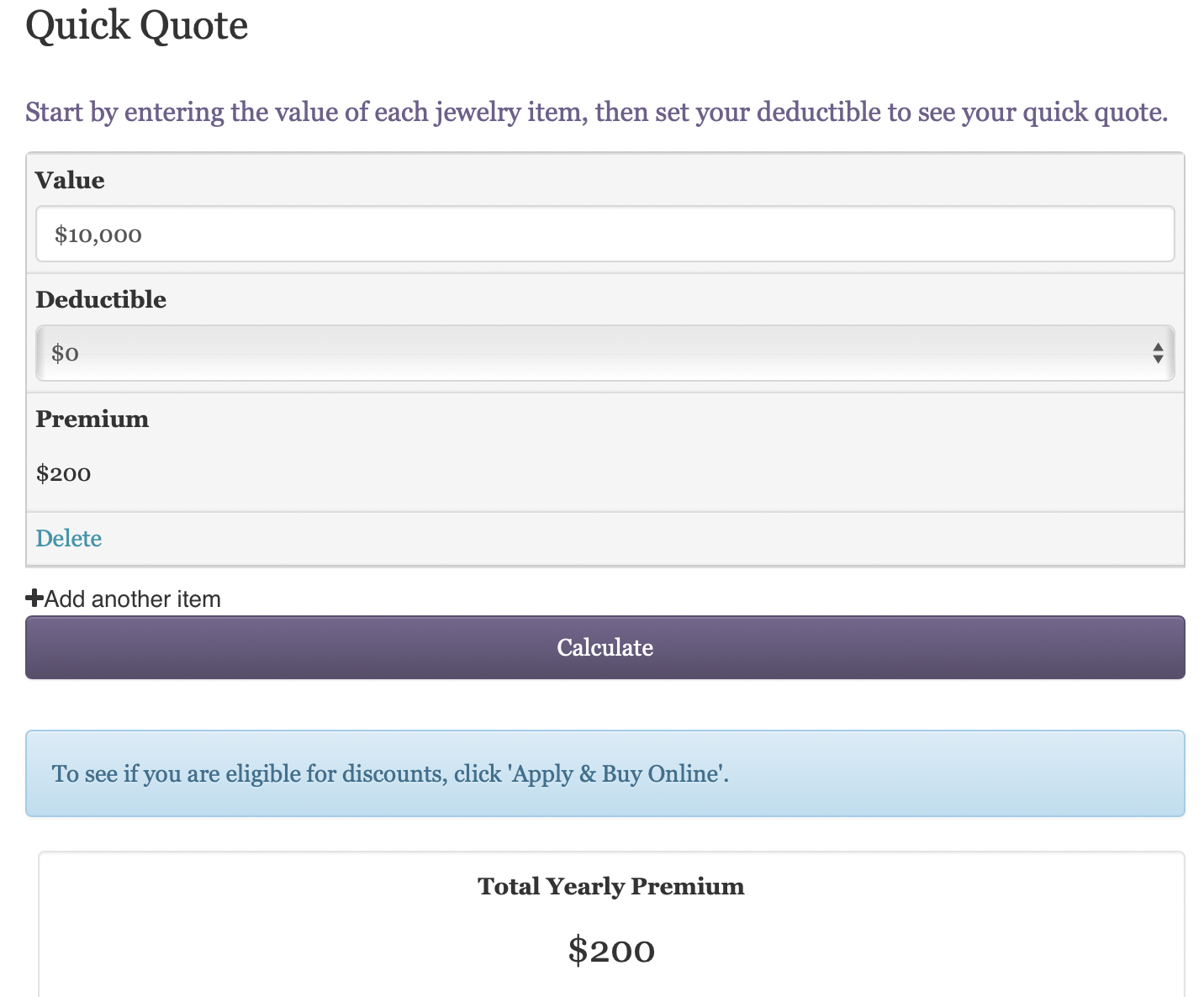

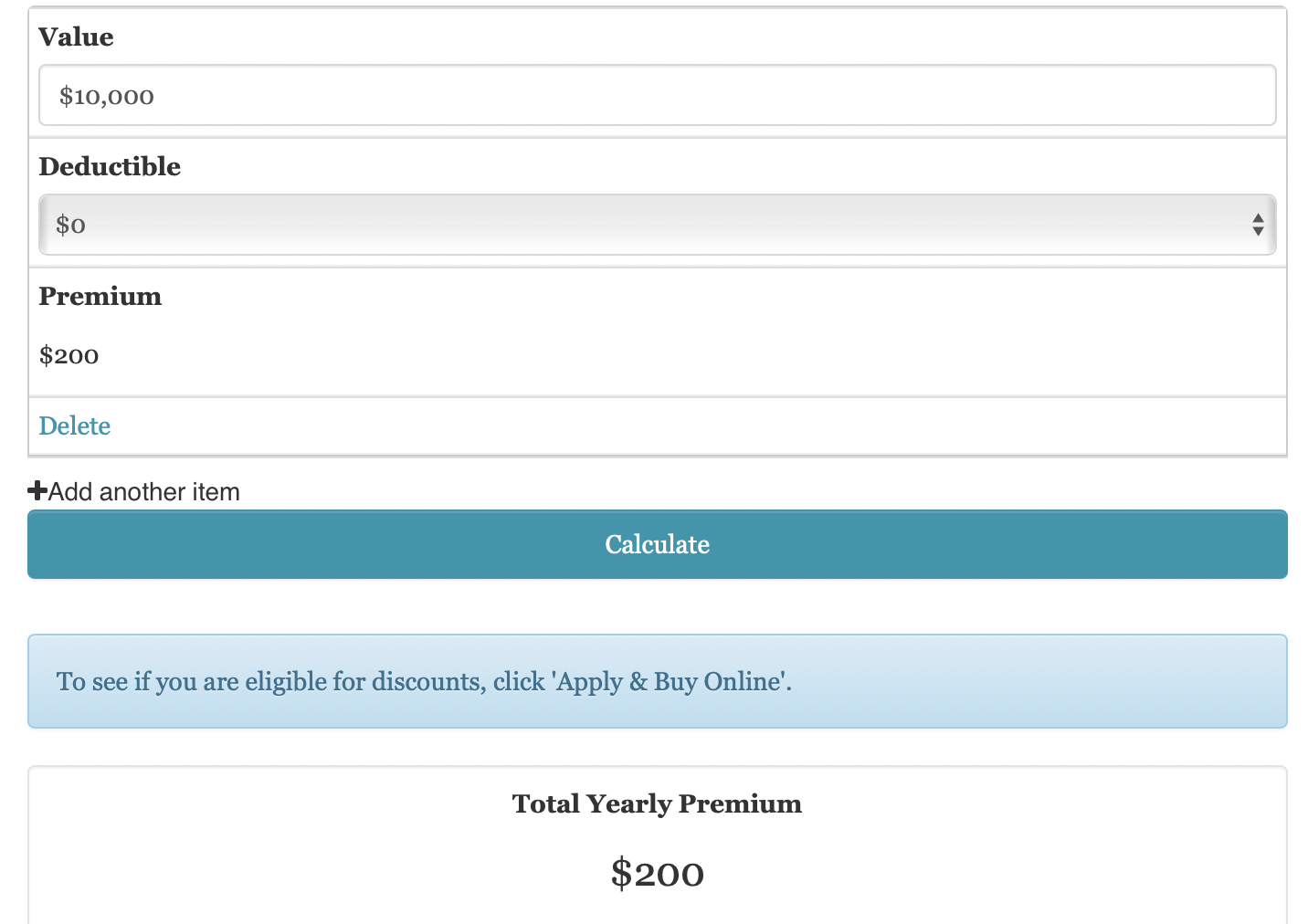

It’s easy to get a quote from Jewelers Mutual; simply enter your zip code and the value of your jewelry. All the quotes are for a $10,000 ring owned by someone in California.

Lavalier: Best for Comprehensive Coverage, including International

Lavalier is also very easy to secure a quote from—all you have to do is enter your zip code where you reside and the value of your jewelry.

International travel is covered, and if you purchase jewelry through Lavalier, it’s automatically insured for up to 30 days. If your jewelry is lost, stolen, or damaged, Lavalier will work with the jeweler of your choice to repair or replace it.

Lavalier gets a B+ from the BBB. Every type of peril is covered, but Lavalier will only insure your jewelry for up to $50,000, so if you have very expensive pieces, you’ll want to look elsewhere, although Lavalier does say they make occasional exceptions.

Zillion: Best If Zillion Works with Your Jeweler

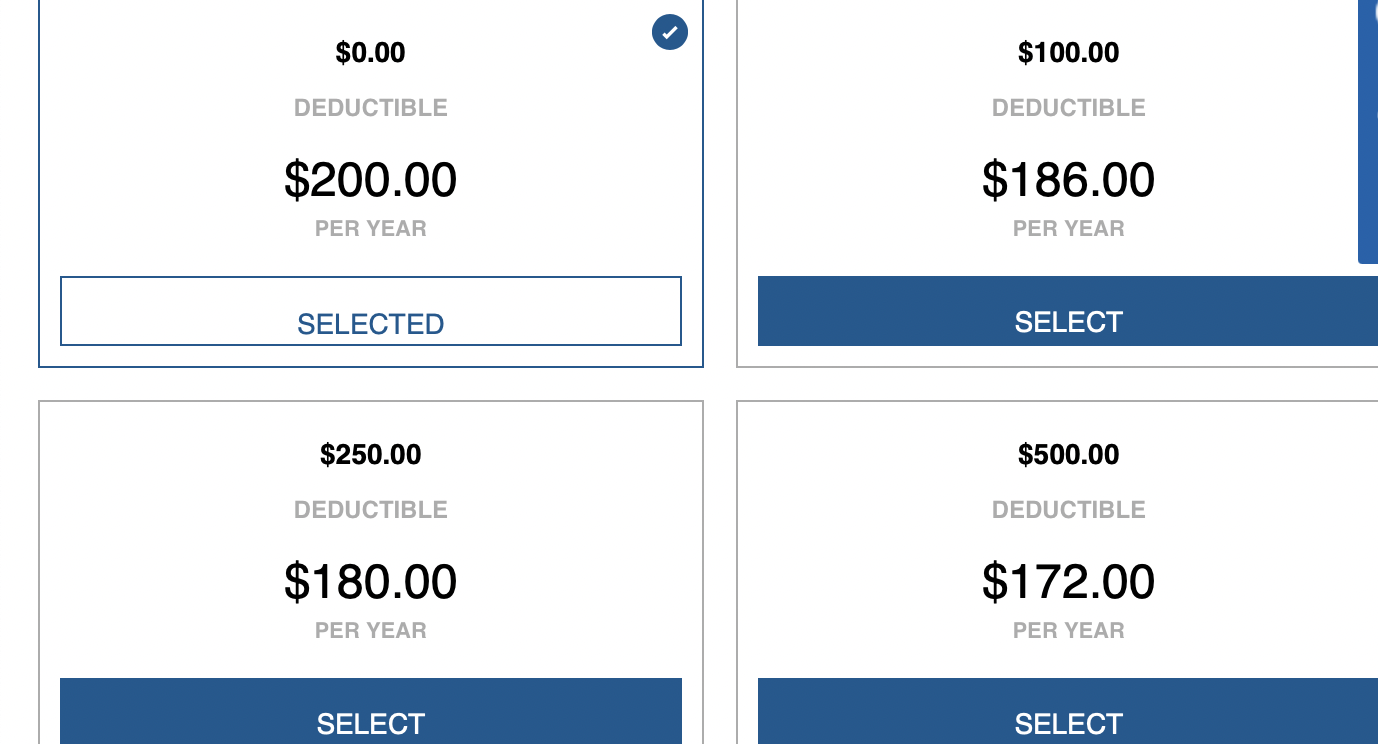

Zillion covers your jewelry against loss, theft, damage, disappearance and natural disasters. They offer a $0 deductible and estimate your cost will be about 1-2% of the replacement value of your jewelry. That means a $10,000 ring could be insured for about $100 a year.

Zillion partners with many jewelers to offer low rates on jewelry insurance. There’s a drop-down menu, and you choose where you purchased your jewelry to get a quote. If the jeweler you purchased your bauble from is not listed, you’re out of luck.

We couldn’t find them on the BBB website, but they have a 4.9 star rating on Trustpilot.

Chubb: Best for High Value Jewelry and Fine Art

Chubb offers insurance of all types, including fine art, wine, and jewelry. They score an impressive A++, or superior, from A.M. Best, which means you never have to worry Chubb won’t have the resources it needs to pay claims. They also offer worldwide coverage with a no deductible option.

If you already have a Chubb policy, new items are automatically covered for up to 90 days. You can also protect your entire collection of fine art, antiques, and jewelry with Chubb. They don’t require an appraisal, just an estimate of the value and the description, unless the piece is valued at over $100,000 (or fine art at more than $250,000).

To get a quote from Chubb, you would have to speak to an agent, so we were unable to obtain a quote.

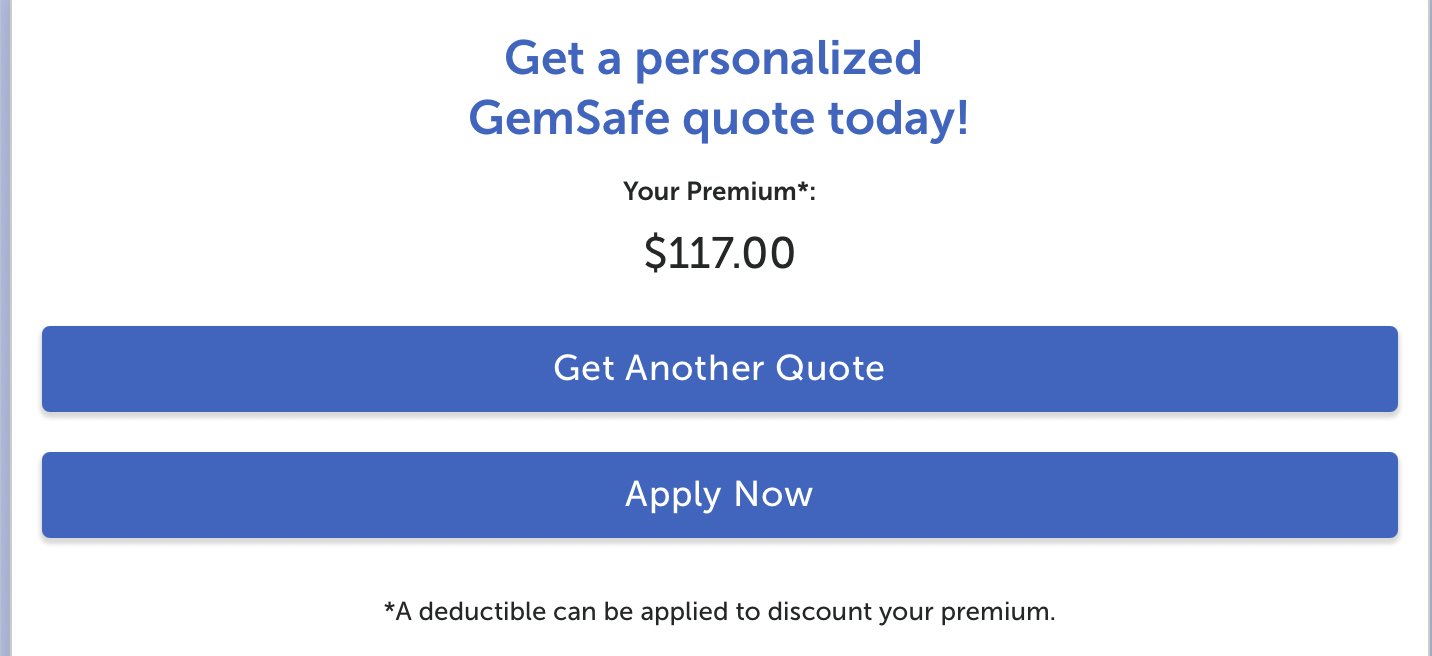

GemSafe: Best for Reappraisal Discounts

If you’re willing to have your jewelry reappraised every year, you can get up to a 3% discount on your policy. GemSafe offers all-risk coverage, which means unless something is specifically excluded, it’s covered.

GemSafe policies are underwritten by SterlingRisk insurance, which is one of the nation’s top 40 independently owned insurance brokerages. It’s easy to get a quote from GemSafe.

One con is that you can’t file a claim online with GemSafe—you have to call.

JIBNA Personal Jewelry Insurance: Best for Personalized Experience

If you like working with agents, or have a lot of questions about jewelry insurance, JIBNA might be for you. They’ll help you navigate what they offer so you can choose the best policy for you. They only insure jewelry and they use patented software to make appraisals. They offer all-risk coverage, which means your jewelry is protected against theft, damage, mysterious disappearances and loss.

Because JIBNA prefers working through agents, you have to call an agent to get a quote. You also have to call your agent to file a claim: you can’t do that online. They also require a $50

Gemshield: Best If You don’t Like Appraisal and Have the Receipts Handy

GemShield protects your jewelry against all risks specific to jewelry—loss, theft, damage, mysterious disappearance and unexplained losses. They also offer replacement coverage. There is also automatic coverage for any new jewelry for up to 30 days. You can then add it to your regular policy.

GemShield doesn’t require appraisals to insure your jewelry, you can just give them the receipts which can expedite the process. They do have a policy limit of $100,000, with a maximum of $35,000 per piece, so if you have a great deal of expensive jewelry, GemShield might not work for you.

If your jewelry is lost or stolen, you can work with their network of jewelers to repair it or replace it. You can get a quote online and make a claim online as well. Coverage is worldwide, which is nice if you travel a lot.

Get quotes for a $10,000 ring in zip code 90230 (California)

How do you obtain coverage for your jewelry?

As an owner of a piece of valuable jewelry, it’s a smart decision to consider getting it insured to protect against potential loss, damage, or theft. Here are some types of insurance coverage you might consider:

Homeowner’s or renter’s insurance:

Your homeowner’s or renter’s insurance policy often includes some coverage for jewelry. However, it’s important to note that these policies typically have a limit for theft of jewelry, which may not cover the full value of more expensive pieces. Coverage also extends to certain named perils only, such as fire or theft, but may not cover all potential causes of loss.

Scheduled personal property coverage (personal articles floater):

This is an add-on coverage to your homeowner’s or renter’s policy that provides higher limits and broader protection for specific, high-value items like jewelry. When you schedule your jewelry, you typically need to provide a recent receipt or appraisal. This coverage often includes “mysterious disappearance,” meaning you’re covered if you lose the item, and there’s typically no deductible.

Jewelry insurance policy:

Companies like Jewelers Mutual offer standalone jewelry insurance policies. These policies usually provide the most comprehensive coverage, protecting against accidental loss, theft, damage, and disappearance. Some will also cover repair or replacement costs.

Before deciding on an insurance policy, it’s crucial to have your jewelry appraised by a professional to determine its actual value. Keep in mind that the value of jewelry can fluctuate over time, so it’s wise to get your pieces reappraised every few years. Always read any insurance policy closely to understand what is and isn’t covered and consider speaking with an insurance professional if you have any questions or concerns.

What coverage do you need for your jewelries?

As a jewelry owner, you’d ideally want an insurance policy that provides comprehensive coverage for your valuable pieces. Here are the types of coverage you might want to consider:

- Theft: This is a common concern for jewelry owners. You want a policy that will cover the full value of your jewelry in case it’s stolen.

- Loss or Mysterious Disappearance: Sometimes, jewelry can get lost or go missing without any clear reason. Insurance that covers this can provide peace of mind.

- Damage: Whether it’s a broken clasp or a loose diamond, damage can happen to any piece of jewelry. Ensure your policy covers repairs or replacements in case of damage.

- Natural Disasters: Events like fires, floods, or earthquakes can put your jewelry at risk. A comprehensive policy should offer coverage for these situations.

- Worldwide Coverage: If you travel often, ensure your coverage extends worldwide. Not all policies cover loss or damage that occurs outside your home country.

- Inflation Protection: As the value of jewelry can increase over time due to inflation, it can be beneficial if your insurance offers some kind of inflation protection, ensuring the amount you’re insured for aligns with the current value of your jewelry.

- Replacement Cost Coverage: Some policies will pay the appraised value of your jewelry if it’s lost or stolen. Others will only pay the actual cash value, which could be less than the replacement cost due to depreciation.

Remember, it’s important to have your jewelry appraised regularly (usually every 2-3 years) to ensure it’s insured for the correct value. Each insurance policy is different, so be sure to carefully review any policy before you sign it to ensure it provides the coverage you need. It’s also a good idea to consult with an insurance professional if you have any questions about what type of coverage is right for you.

Does a rider on my homeowners insurance or renters’ insurance policies provide all of these coverages?

A rider, also known as an endorsement or floater, can be added to your homeowners or renters insurance policy to provide additional coverage for specific, valuable items like jewelry. However, the coverage offered by a rider can vary widely depending on the insurance company and the specifics of the policy.

In general, a rider can provide some or all of the following types of coverage:

- Theft: Most riders will cover the theft of the jewelry piece, often up to its appraised value. It’s also important to note that these policies typically have a limit for theft of jewelry, which may not cover the full value of more expensive pieces.

- Loss or Mysterious Disappearance: Some riders will cover loss or mysterious disappearance, but this isn’t always included. You’ll need to check the specifics of your policy.

- Damage: Coverage for damage can depend on the specifics of the policy. Some riders will cover damage, while others may not.

- Natural Disasters: Depending on your location and the terms of your policy, your rider may or may not cover damage from natural disasters.

- Worldwide coverage: Riders often provide coverage no matter where the loss or damage occurs, but again, this can depend on the specifics of your policy.

Riders may not provide coverage for inflation protection or replacement cost. This means that if the value of your jewelry has increased since it was last appraised, your rider may not provide enough coverage to replace it if it’s lost or stolen.

It’s important to note that riders often come with a separate deductible, which means you’ll need to pay out-of-pocket before the insurance coverage kicks in.

When considering whether to add a rider to your homeowners or renters policy, it’s crucial to read the fine print and understand exactly what’s covered. You should also have your jewelry appraised regularly to ensure it’s insured for the correct value. If the coverage provided by a rider doesn’t meet your needs, you may want to consider a standalone jewelry insurance policy.

How much does jewelry insurance cost?

Obviously, comprehensive jewelry insurance costs depends on several factors which we will be discussing the details below. The value of the jewelries is the most important factor affecting the cost.

For a $10,000 piece of jewelry, the annual average cost is $146. Most policies from the providers we recommend above cost between $100 to $200 a year. They all have a bit differences in coverages, so be sure to study the policy’s coverage well before making your decision.

What factors affect the jewelry insurance cost?

Below are the main factors affecting jewelry insurance cost:

Value of the jewelry

One of the primary factors that impact the cost of personal jewelry insurance is the value of the jewelry. The higher the value, the more you’ll likely have to pay for coverage. An appraisal will typically be required to establish the value of the piece. This appraisal should ideally be conducted by a certified professional and include detailed information about the piece, such as the cut, clarity, carat, and color of any gemstones, the weight of any precious metals, and the presence of any unique or identifiable features.

Type of coverage

The type of coverage you choose will also impact the cost of your insurance. Policies that cover a broader range of risks (all-risk coverage) will typically be more expensive than those that only cover specific perils (named-peril coverage). Similarly, policies that offer replacement cost coverage (which pays the amount necessary to replace the item) will typically cost more than those that only offer actual cash value coverage (which pays the item’s depreciated value).

Deductible

The deductible you choose for your policy can significantly impact your insurance costs. A higher deductible (the amount you pay out of pocket before the insurance company begins to cover costs) typically results in lower premiums. However, you must be comfortable paying this amount in the event of a loss.

Location and usage

Where you live and how you use the jewelry can also impact the cost of coverage. If you live in an area with higher rates of theft or loss, or if you frequently wear the jewelry in public, you may have to pay more for insurance.

Security measures

Insurance companies often take into account the security measures you’ve put in place to protect your jewelry. This could include things like owning a home safe or storing the jewelry in a bank safe deposit box when it’s not being worn. The more robust your security measures, the lower your insurance costs might be.

Claims history

Just like with other types of insurance, your claims history can impact the cost of personal jewelry insurance. If you’ve made previous insurance claims, especially recent ones, you may be seen as a higher risk and be required to pay more for coverage.

Remember, it’s important to thoroughly understand your insurance policy, including what is and isn’t covered, so you can make an informed decision about what type of coverage is best for you.

How to find cheap jewelry insurance?

Securing your precious jewelry doesn’t have to be a costly affair. There are several strategies to find affordable yet comprehensive insurance coverage for your valuable pieces. By understanding how insurance pricing works and how to leverage different factors, you can potentially lower your premium while ensuring your jewelry gets the protection it deserves. In this section, we will delve into six key tips to help you find cheap jewelry insurance.

Compare quotes

One of the most effective ways to find cheap jewelry insurance is by comparing quotes from multiple insurance providers. You can either do this manually, or you can use an online comparison tool. Keep in mind that the cheapest policy isn’t always the best one – it’s important to make sure you’re getting the right amount of coverage for your needs.

Consider your deductible

The amount of your deductible can greatly influence the cost of your insurance. In general, the higher your deductible, the lower your premium will be. However, make sure that you choose a deductible that you can afford to pay out of pocket in the event of a claim.

Improve security

Insurance companies often offer discounts to policyholders who take measures to protect their jewelry. This could include storing your jewelry in a safe when it’s not being worn, installing a security system in your home, or even keeping your jewelry in a safety deposit box at the bank. Be sure to ask potential insurers about any discounts they might offer.

Maintain a clean claims history

Insurers often offer lower premiums to those with a clean claims history. This is because a history of making insurance claims can indicate that you are a high-risk policyholder. Therefore, being careful with your jewelry and avoiding unnecessary claims can help you secure cheaper coverage.

Consider standalone coverage

While adding a rider to your homeowners or renters insurance can be a convenient way to insure your jewelry, it might not always be the cheapest option. Standalone jewelry insurance policies often offer more comprehensive coverage and can sometimes be more affordable. Be sure to compare the costs of both options before making a decision.

Annual reevaluation

It’s wise to annually reevaluate the value of your jewelry and the coverage of your policy. The market price for precious metals and gemstones fluctuates, and the value of your jewelry may decrease, leading to potential savings on your premiums.

Remember, finding cheap jewelry insurance isn’t just about finding the lowest premium. It’s about finding a policy that offers the right level of coverage for your needs at a price you can afford.

What is jewelry store insurance? How is it different from personal jewelry insurance?

Jewelry store insurance is a type of business insurance specifically designed to protect jewelry stores from a variety of risks associated with their operations. This insurance typically covers risks such as theft or damage of inventory (jewelry), property damage to the store itself, liability if a customer is injured on the premises, and even business interruption insurance if the store needs to close temporarily due to a covered loss.

On the other hand, personal jewelry insurance is for individuals who own jewelry. This type of insurance primarily covers the jewelry items owned by a person, rather than a business. It is designed to protect against risks such as theft, loss, or damage of personal jewelry items. It doesn’t include coverages necessary for running a business, like liability or business property damage.

In essence, the key difference is that jewelry store insurance is designed for the needs of a jewelry business, while personal jewelry insurance is intended for individuals seeking to protect their personal jewelry collection. Both types of insurance provide coverage for jewelry, but the context in which the jewelry is covered (business vs. personal) and the additional coverages included make them suitable for different purposes.

FAQs about personal jewelry insurance

What is personal jewelry insurance?

Personal jewelry insurance is a specific type of coverage that protects your valuable pieces, such as rings, watches, and necklaces, against loss, theft, damage, or even mysterious disappearance. It can be purchased as a standalone policy or as a rider to your homeowners or renters insurance.

Do I need an appraisal for personal jewelry insurance?

Most insurance companies will require an appraisal for high-value items to determine the worth of the jewelry piece and subsequently the amount of coverage needed. This is typically required for pieces valued over a certain threshold, usually around $1,000-$2,000.

Does homeowners or renters insurance cover my jewelry?

While homeowners and renters insurance typically includes coverage for personal belongings, including jewelry, the limits are usually relatively low and may not fully cover high-value pieces. Furthermore, they may not cover all types of losses (like accidental loss). That’s where specific jewelry insurance or a jewelry rider comes in handy.

Are all types of jewelry covered under personal jewelry insurance?

Generally, personal jewelry insurance covers all types of jewelry, including rings, bracelets, necklaces, watches, and earrings. However, each insurance company may have different policies, and some may exclude certain types of items. Always check with your insurance provider to understand exactly what is covered.

What if my jewelry item is a family heirloom or has sentimental value?

While insurance can provide financial compensation if something happens to your jewelry, it can’t replace the sentimental value of a family heirloom. However, having insurance coverage can give you peace of mind and help you restore or replace the item if it’s lost or damaged. It’s important to get an accurate appraisal of the item’s value to ensure you have enough coverage.